.jpg)

(Reuters) – The U.S. economy unexpectedly contracted in the first quarter amid a resurgence in COVID-19 cases and drop in pandemic relief money from the government, but the decline in output is misleading as domestic demand remained strong.

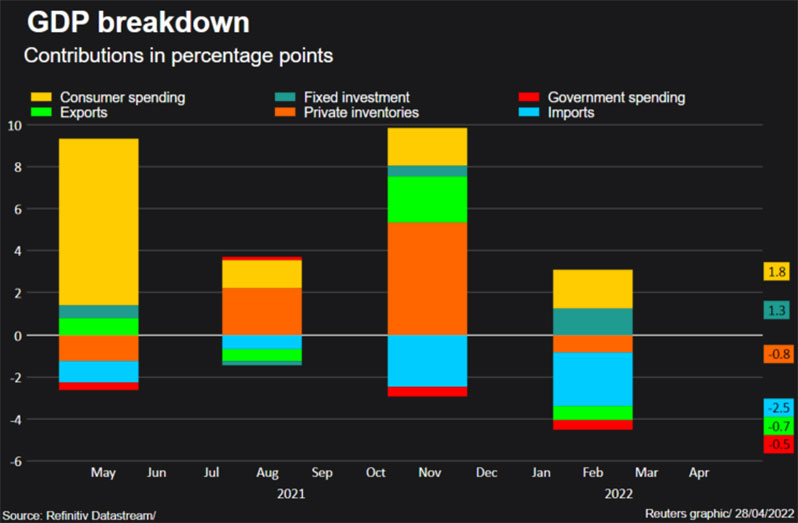

The first decrease in gross domestic product since the short and sharp pandemic recession nearly two years ago, reported by the Commerce Department on Thursday, was mostly driven by a wider trade deficit as imports surged, and a slowdown in the pace of inventory accumulation.

A measure of domestic demand accelerated from the fourth quarter’s rate, allaying fears of either stagflation or a recession. The Federal Reserve is expected to hike interest rates by 50 basis points next Wednesday. The U.S. central bank raised its policy interest rate by 25 basis points in March, and is soon likely to start trimming its asset holdings.

“The economy is still showing some resilience, but the first-quarter GDP report signals the start of more moderate growth this year and next, largely in response to higher interest rates,” said Sal Guatieri, a senior economist at BMO Capital Markets in Toronto. “Despite the contraction, the Fed has little choice but to hike aggressively in May to corral inflation.”

Gross domestic product fell at a 1.4 per cent annualised rate last quarter, the government said in its advance GDP estimate. The economy grew at a robust 6.9 per cent pace in the fourth quarter. Economists polled by Reuters had forecast GDP growth rising at a 1.1 per cent rate. Estimates ranged from as low as a 1.4 per cent rate of contraction to as high as a 2.6 per cent growth pace.

The economy also took a hit from supply-chain challenges, worker shortages and rampant inflation. Last quarter’s decline is a head fake as GDP remains 2.8 per cent above its level in the fourth quarter of 2019 and the economy grew 3.6 per cent on a year-on-year basis. Further, 1.7 million jobs were created in the first quarter and manufacturing output grew at a five per cent pace.

“It is nonsense that real GDP declined,” said Conrad DeQuadros, senior economic adviser at Brean Capital in New York.

But the mismatch hints at weaker productivity last quarter.

Front-loading by businesses fearful of shortages because of the Russia-Ukraine war contributed to a surge in imports. Exports tumbled, leading to a sharp widening of the trade deficit, which chopped 3.20 percentage points from GDP growth, the most since the third quarter of 2020. Trade has now been a drag on growth for seven straight quarters.

Front-loading by businesses fearful of shortages because of the Russia-Ukraine war contributed to a surge in imports. Exports tumbled, leading to a sharp widening of the trade deficit, which chopped 3.20 percentage points from GDP growth, the most since the third quarter of 2020. Trade has now been a drag on growth for seven straight quarters.

Businesses have turned to imports to satisfy demand, with local manufacturers lacking the capacity to boost production. Business inventories increased at a $158.7 billion pace, slowing from the robust $193.2 billion rate in the October-December quarter. Inventory investment cut 0.84 percentage point from GDP growth.

Stocks on Wall Street were higher as investors shrugged of the drop in GDP. The dollar rose against a basket of currencies. U.S. Treasury prices fell.

Growth in consumer spending, which accounts for more than two-thirds of U.S. economic activity picked up at a rate of 2.7 per cent from the fourth-quarter’s 2.5 per cent pace, despite taking a hit from the winter wave of coronavirus cases, driven by the Omicron variant.

The loss of pandemic money to households from the government was partially offset by rising wages amid a tightening labuor market. Government spending fell for a second straight quarter.

Strengthening labour market conditions were reinforced by a separate report from the Labour Department on Thursday showing initial claims for state unemployment benefits fell 5,000 to a seasonally adjusted 180,000 for the week ended April 23. With a near record 11.3 million job openings at the end of February, employers are desperately hanging on to their workers.

Even with food and gasoline prices soaring, there is no sign yet of consumers pulling back. The government’s measure of inflation in the economy surged at a 7.8 per cent rate, the fastest in 41 years, after increasing at a 7.0 per cent pace in the fourth quarter. Inflation by all measures has overshot the Fed’s two per cent target.

At least $2 trillion in excess savings accumulated during the pandemic are providing a cushion against inflation.

Workers’ shortages saw businesses boosting investment, with spending on equipment increasing at a 15.3 per cent rate last quarter. They mostly bought computers and industrial machinery.

That combined with solid consumer spending to hoist final sales to private domestic purchasers at a 3.7 per cent rate. This measure of domestic demand, which excludes trade, inventories and government spending, increased at a 2.6 per cent rate in the fourth-quarter. Final sales to private domestic purchasers account for roughly 85 per cent of aggregate spending.

The housing market notched another second straight quarterly gain, but with the 30-year fixed mortgage shooting above five per cent, the outlook is uncertain.

While concerns remain that the Fed could aggressively tighten monetary policy and tip the economy into recession, most economists are not convinced, pointing to the strong domestic demand and signs that inflation may have peaked.

Consumer spending last quarter was driven by services. The shift in demand from goods is likely to help ease pressure on supply chains, though the coronavirus-related lockdowns in China pose a risk.

“The U.S. economy is not anywhere close to recession,” said Gus Faucher, chief economist at PNC Financial in Pittsburgh, Pennsylvania. “Underlying demand remains strong, and the labor market is in excellent shape. Growth will resume in the second quarter.”