.jpg)

Is the paradoxical Dutch Disease present? (Part II)

Discussion and Analysis

Real GDP Growth

Real GDP Growth

ACCORDING to the Mid-Year 2022 economic report, the economy recorded real GDP growth of an estimated 36.4 per cent, driven by the petroleum, other crops, and services sectors. Moreover, despite the setbacks that affected the other sectors, the non-oil economy recorded positive growth for the half- year period of an estimated 8.3 per cent. As such, the Ministry of Finance is confident that with the measures in place to continue increased economic activity, overall GDP growth for 2022 is now forecast to grow by 56 per cent, and non-oil growth by 9.6 per cent.

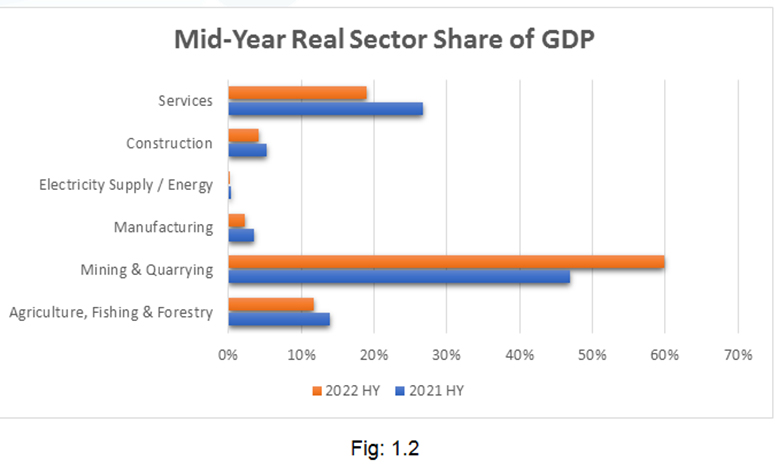

Sectorial Performance

Sectorial Performance

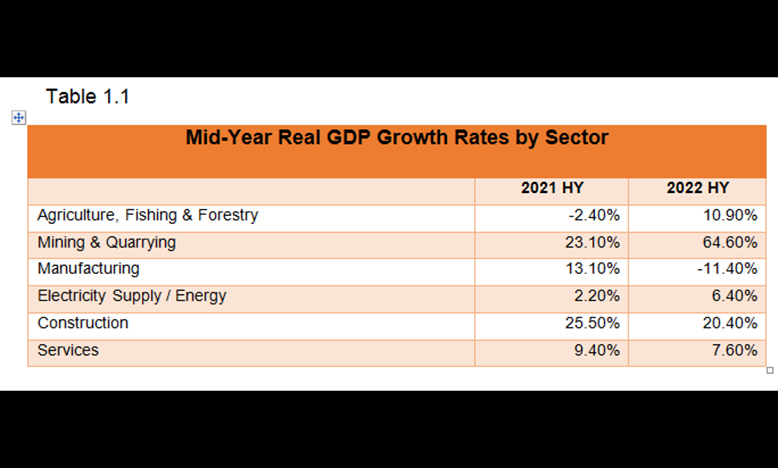

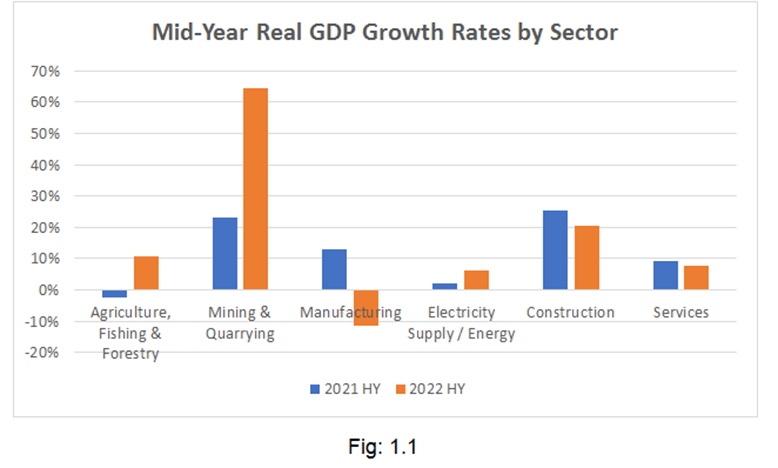

The non-oil economy has shown positive signs of recovery on account of the Government’s accommodative fiscal policy stance and allocation of resources aimed to repair the non-oil sectors – having suffered deteriorated performance in 2020 and 2021, and arguably the period 2015 – 2020. The agriculture, forestry and fishing subsector recorded growth of 11 per cent for the first half of the fiscal year (FY) 2022 compared to a negative growth of two per cent for the corresponding half year period in 2021.

The mining and quarrying subsector, energy, construction, and services subsectors also recorded positive growth for the first half of FY 2022 of 65 per cent, six per cent, 20 per cent and eight per cent respectively. Conversely, the manufacturing subsector declined by 11 per cent when compared to the corresponding period in 2021 on account of increased input costs and lower output for other manufacturing and pharmaceutical and medical products.

The mining and quarrying subsector, energy, construction, and services subsectors also recorded positive growth for the first half of FY 2022 of 65 per cent, six per cent, 20 per cent and eight per cent respectively. Conversely, the manufacturing subsector declined by 11 per cent when compared to the corresponding period in 2021 on account of increased input costs and lower output for other manufacturing and pharmaceutical and medical products.

The sugar and rice manufacturing sector declined by 55.9 per cent and 17.3 per cent respectively, which is consistent with the lower output of both commodities as reported under the agricultural sub sectors of these commodities. The rice and sugar subsectors experienced lower output on largely account of the setback due to the floods and inclement weather patterns.

Notwithstanding, the wholesale, retail and trade, and entertainment subsectors recorded higher growth compared to the previous corresponding period. This is evidenced of the positive impact of Government’s intervention in the economy to cushion the impact of rising cost of living, such as the various cash grants and other measures.

Notwithstanding, the wholesale, retail and trade, and entertainment subsectors recorded higher growth compared to the previous corresponding period. This is evidenced of the positive impact of Government’s intervention in the economy to cushion the impact of rising cost of living, such as the various cash grants and other measures.

External Trade

External Trade

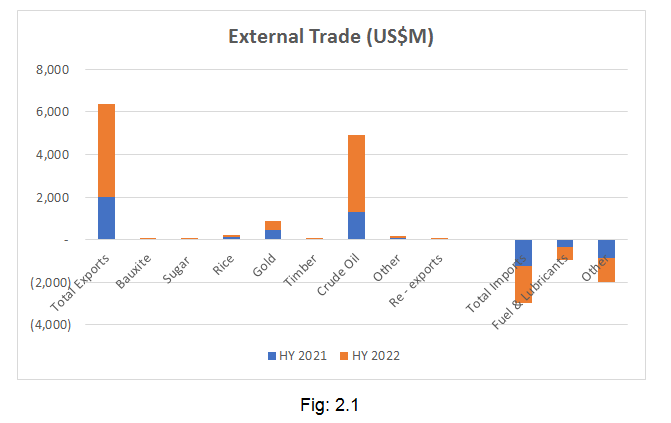

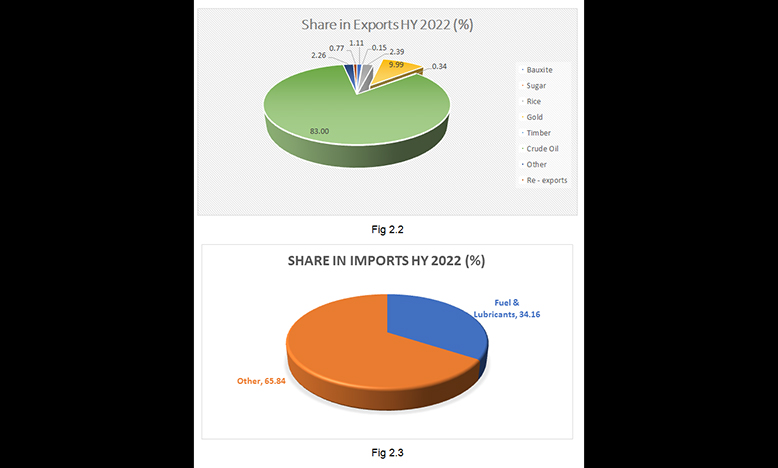

Total exports for the first half year period of FY 2022 increased nominally by 115 per cent driven largely by crude oil which increased by 179 per cent. Export of bauxite increased by 18 per cent, timber increased by 26 per cent, other exports increased by 15 per cent and re-exports increased by 123 per cent. Conversely, sugar, rice and gold declined by 39 per cent, 16 per cent and 0.8 per cent respectively. On the other hand, total imports increased by 41 per cent of which fuel and lubricants increased by 63 per cent on account of higher prices and other imports increased by 32 per cent.

Figures 2.2 and 2.3 above illustrate the share of total exports and imports for the first half of FY 2022, wherein export of crude oil production accounted for 83 per cent of total exports while other exports accounted for 17 per cent of total exports. In terms of imports, import of fuel and lubricants accounted for 34 per cent of total imports while other imports accounted for 66 per cent of total imports.

Figures 2.2 and 2.3 above illustrate the share of total exports and imports for the first half of FY 2022, wherein export of crude oil production accounted for 83 per cent of total exports while other exports accounted for 17 per cent of total exports. In terms of imports, import of fuel and lubricants accounted for 34 per cent of total imports while other imports accounted for 66 per cent of total imports.

Credit to the Private Sector and the Money Supply

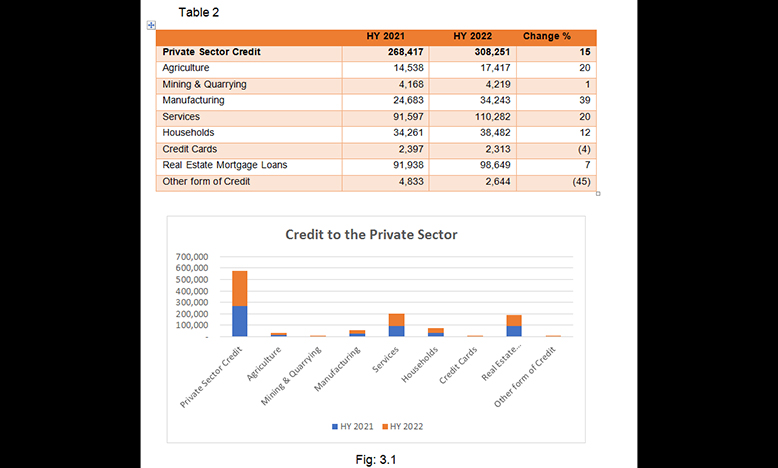

Credit to the private sector increased by 15 per cent relative to the previous half year period in FY 2021. This increase was driven by increased credit to the agriculture sector by 20 per cent, mining and quarrying sector by one per cent, manufacturing sector by 39 per cent, services sector by 20 per cent, households by 12 per cent and real estate mortgages by seven per cent. This is indicative of broad-based growth through private sector investment across all the major non-oil sectors. Conversely, credit cards declined by four per cent and other forms of credit by 45 per cent.

The total money supply expanded by 14 per cent as well as shown in figure 3.2 from $541 billion for the half year period January – June 2021 to $616 billion for the half year period January – June 2022.

Inflation

Inflation

The revised inflation forecast for the end of 2022 is 5.8 per cent which is below the global average forecast for 2022 of 8.2 per cent.

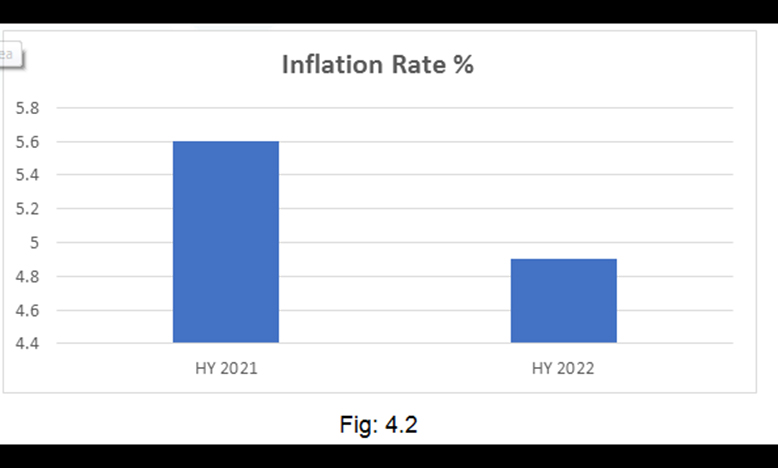

Notably, the inflation rate for the half year period January – June 2022 of 4.9 per cent is lower than the 5.6 per cent for the previous corresponding period in 2021. This is evidenced of the impact of Government interventions to cushion the rising inflation rate on account of inflationary pressures stemming from the global economy.

Notably, the inflation rate for the half year period January – June 2022 of 4.9 per cent is lower than the 5.6 per cent for the previous corresponding period in 2021. This is evidenced of the impact of Government interventions to cushion the rising inflation rate on account of inflationary pressures stemming from the global economy.

Exchange Rate

Exchange Rate

The exchange rate appreciated marginally by 0.91 per cent from $208.8 for the first half year period in FY 2021 to $206.9 for the first half year period FY 2022.

Banking Sector Net Foreign Assets and Foreign Reserves

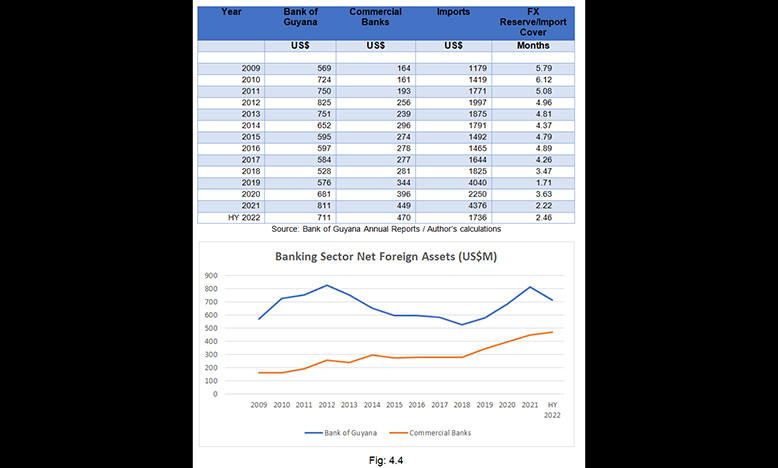

The Bank of Guyana foreign exchange (FX) reserve balance which stood at US$711 million for the period ended January – June 2022, represented 2.46 months import cover. The FX reserve weakened steadily during the period 2015 through 2020 in terms of its equivalency relative to the minimum requirement of import cover – that is, three months’ worth of import cover. In 2009 the FX reserve represented 5.79 months of import cover, 6 months import cover in 2010, 5 months import cover in 2011 – 2013, more than 4 months import cover in 2014 and close to 5 months import cover up to 2016.

From 2017 – 2020 the FX reserve started to weaken below 4.5 months of import cover down to 3.4 months import cover in 2018, 1.7 months import cover in 2019 and 2.2 months import cover in 2020.

From 2017 – 2020 the FX reserve started to weaken below 4.5 months of import cover down to 3.4 months import cover in 2018, 1.7 months import cover in 2019 and 2.2 months import cover in 2020.

Despite this, the exchange rate remained stable because fortunately, the net foreign assets (NFA) of the commercial banks (which are the dominant players in the FX market) experienced dramatic increases during the twelve years’ period spanning 2009 to 2021 and thus remained strong. In this respect, while the Bank of Guyana FX reserves increased by 43 per cent over this period from its 2009 position of US$569 million to US$811 million by the end of 2021; the commercial banks NFA increased by 174 per cent from US$164 million in 2009 to US$449 million by the end of 2021. This outturn is largely due to increased foreign direct investments, growth in the private sector FX balances, and growth in overseas investments by the local financial institutions.

Public Debt Management

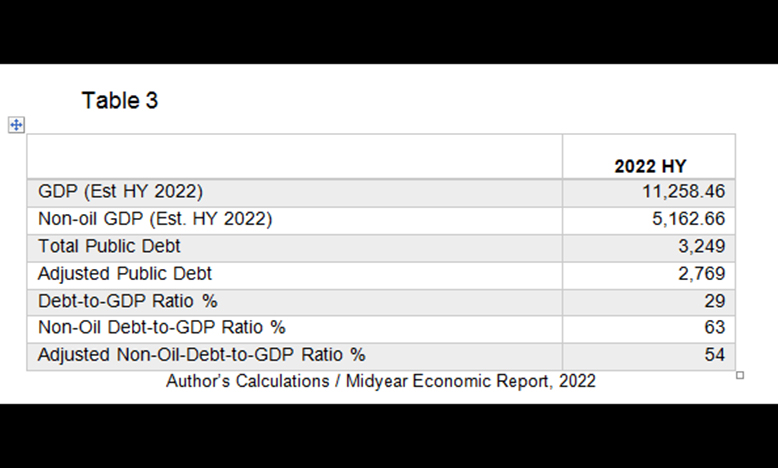

According to the mid-year economic report for the first half of FY 2022, the overall economy is estimated to have grown by 36.4 per cent and the non-oil economy by 8.3 per cent. The total stock of public debt for the period is reported to at US$3.249 billion. Applying the estimated rate of growth in real GDP terms to FY 2021 real GDP – this can be used to calculate the debt-to-GDP ratio and non-oil debt-to-GDP ratio for the first half of FY 2022.

Having so done, the debt-to GDP ratio stood at an estimated 29 per cent for the first half of FY 2022 and the non-oil debt to GDP ratio an estimated 63 per cent for the period. Both of these ratios indicate that the level of public debt is relatively low to moderate in terms of the risk of default. This is despite the massive increase in public expenditure especially towards capital expenditure which is partly due to about 23 per cent of the 2022 budget being financed through the first drawdown from the Natural Resource Fund (NRF).

Having so done, the debt-to GDP ratio stood at an estimated 29 per cent for the first half of FY 2022 and the non-oil debt to GDP ratio an estimated 63 per cent for the period. Both of these ratios indicate that the level of public debt is relatively low to moderate in terms of the risk of default. This is despite the massive increase in public expenditure especially towards capital expenditure which is partly due to about 23 per cent of the 2022 budget being financed through the first drawdown from the Natural Resource Fund (NRF).

Moreover, it is worthwhile to examine the debt-to-GDP ratio from another perspective where another adjustment is perhaps imperative. During the period 2015 – 2020, the previous Administration racked up an overdraft of about $100 billion in the Government deposit accounts at the Bank of Guyana. This practice, as was flagged by the Auditor General Report, was in contravention of the Fiscal Management and Accountability Act. In this regard, section 60 of the Act speaks to “overdraft facility” where it states that “the Minister shall repay in full all advances in the form of an overdraft on all official bank account on or before the end of the fiscal year during which that overdraft was drawn”.

Further to note, the overdraft balances were never reported as part of the public stock of debt during the period 2015 – 2020. Hence, should this overdraft amount be excluded from the stock of debt of $100 billion, the non-oil debt to GDP ratio would have been around 54 per cent and overall debt to GDP ratio below 29 per cent.

This partly explains the reason why the current Minister with responsibility for Finance, Dr. Ashni Singh had to seek the National Assembly’s approval to raise the public debt ceiling so as to now regularize the Government Deposit Accounts by clearing the overdraft balances and adding same onto the official stock of public debt.

Notwithstanding, with the expansive development trajectory of the economy and the low debt to GDP ratio suggests that the level of public debt is quite sustainable with a low to moderate default risk, and the Administration of the day must be commended for this type of prudent public debt management by restricting the temptation to borrow excessively against future oil revenues.

In the interest of absolute clarity, it must be noted that while the GDP growth is largely driven by the activities in the oil and gas sector and the support services sector, borrowing against future (projected) oil revenues is a slightly different issue altogether, which is a dangerous path to pursue. The Government has so far avoided going this route which is fiscally prudent and commendable.